The Importance of National Domestic Violence Awareness Month

September 20, 2022

The Impact of the 2022 Hurricane Season

October 24, 2022October 18, 2022

Whether an organization provides direct corporate assistance or has a private foundation, financial assistance being given to a team member must comply with tax-exempt regulations.

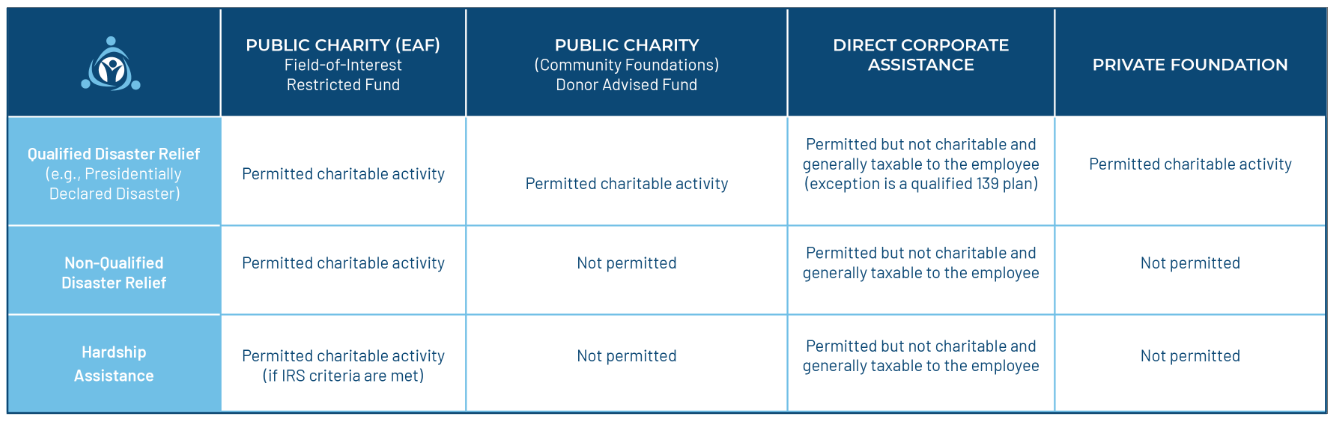

Public charities with Field-of-Interest Funds, like Emergency Assistance Foundation, are permitted to provide tax-advantaged relief for qualified disasters, non-qualified disasters, and hardships, while Community Foundations, Direct Corporate Assistance, and Private Foundations are not. The chart below outlines the various charitable structures and their abilities to provide relief based on regulations.

Here are 5 common things to look for when determining if a relief fund is out of compliance and some ways to ensure compliance:

1. Are the fund’s grant guidelines specific and objective?

Issues occur when grant guidelines are very general and/or when grant decisions are made subjectively. According to IRS regulations, “[t]he organization establishes specific written criteria for the application, selection and disbursement of funds.” For example, including “other” as an option in any of the grant criteria is not specific. A straightforward way to determine if the grant guidelines are specific and objective is to ask yourself if the application was reviewed by 5 different people, would they all come to the same conclusion?

2. Is an advisory/oversight committee being used appropriately?

Organizations often use a committee of team members and/or retired team members to administer a fund, which often results in an inconsistent process that is not objective. IRS Regulations state that “[t]he organization establishes a committee to administer the program consisting of persons who aside from serving on the committee have no financial interest in the employer; or the committee consists of persons representing a broad spectrum of employees who understand that they are acting in a personal capacity as agents of the organization rather than as representatives of the employer.”

For example, if grant recipients are selected by management or human resources, the IRS would not view this as an independent, objective process. One way to guarantee maximum independence is to partner with a third-party public charity that has disaster and hardship relief expertise.

3. Is employment used only as an initial qualifier for eligibility?

While employment can be used as an initial qualifier for eligibility to apply for and receive a grant, additional measures like requiring a supervisor's signature on the application, considering disciplinary issues, or considering a team members length of service, etc. should not be included.

IRS guidelines state that “[t]he conditions are designed to ensure that employment is merely an initial qualifier for eligibility, that the ultimate recipients are not chosen based upon employment related factors, and that those responsible for selecting recipients are independent from the employer.”

Beyond initial eligibility, the nexus between employer and employee must be deemed broken. This can be accomplished by utilizing a third-party public charity like EAF because the applicant is seen as an individual rather than an employee or contractor, and the grants are not excessively controlled by the sponsoring organization.

4. Is the fund structured and administered in a way to ensure full regulatory compliance?

Most funds attempt to comply with federal and state regulations, but do not fully understand the depths of compliance. The most common way funds do not comply fully with regulations is by providing a private benefit to parties administering the program, which means that the IRS may view the program as a team member benefit which is advantageous to the organization. The IRS’s main concern is that relief funds do not “impermissibly serv[e] the related employer” which means that that the fund is not a disguised benefit or compensation.

One way to ensure regulatory compliance is to only provide disaster relief grants to individuals affected by qualified disasters. Another way to do this is to have the relief fund program run as a public charity rather than a private foundation so that the organization is less involved in the funding and administering of the program.

5. Is the fund structured and communicated in a way to ensure full regulatory compliance?

IRS publications require that “[t]he organization informs all charitable class members that disaster relief and emergency hardship funds are available, including the criteria for application and selection.”

Many organizations try their best to ensure that a program is communicated to all team members, but often this is not done well. For example, if new team members are made aware that there is a relief fund program available to them, but grant criteria is not shared – this is less compliant. Ongoing, effective communication to keep team members updated on the state of the fund on a regular basis and celebrating the funds success are two great ways to keep team members involved.

If your organization is interested in starting a relief fund or ensuring a current fund’s compliance, consider scheduling a meeting with Emergency Assistance Foundation.

Author: Doug Stockham, President

Emergency Assistance Foundation

{kind=link}

{kind=link}

{kind=link}